The Rise of Fintech Companies

Do you understand these fintech companies?

Fintech companies are making traditional banks a utility rather than a gatekeeper.

A simple example of this would be, let’s go back to 2005. You are a startup and need help with a bank to accept payments, manage expenses, and track where the money is moving in your company. Now the only option you have is “Partner with a bank.”

You need to head over to the bank branch, meet the bank manager, submit the paperwork, negotiate the deal, and wait months for the approval. Good luck with that. On top of that, issuing a corporate card is literally a nightmare because that requires another level of credibility.

You see what I mean?

Lack of financial accessibility and infrastructure for businesses was one of the major reasons startups would get buried in the void. I mean literally, go ask anyone who ran businesses in the early 2000s, they’ll tell you how hard things were.

Fast forward today, the friction is still there but things have gotten much better.

Fintech companies like Stripe single-handedly solved some of the most common problems of startups, like accepting payments, paying contractors and vendors, issuing corporate cards, and more. But Stripe isn’t the only one in the race. In the last decade or so, a ton of fintech startups have emerged. You may have already heard about companies like Chime, Mercury, Brex, Plaid, Ramp, Revolut, and others.

There's been a rise of fintech startups in recent years, which is a good thing because they make things simpler, faster, cheaper, and more efficient. However, the problem I think is that most people don’t quite understand what these fintech startups are about and what they actually do.

Not good, right? Every single founder and leader should know about these emerging fintech startups, not because you want to know them, but because you may need them to run your company. So, to increase awareness, I thought of writing about these fintech companies.

Just to be clear, I’m not affiliated or partnered with any of the following companies. I think they are doing an amazing job that I just want to share with you. I’ll walk you through what these fintech companies are about, what exactly they do, and the valuation & total user base they have.

Let’s dive in!

Stripe

After selling their first company, Auctomatic for $5 million, Patrick and John Collison started Stripe in 2010. The reason they started? They realized how hard it was, especially for indie hackers and developers to accept payments online. It was a massive pain that they wanted to solve and thought of building Stripe.

Soon, Stripe became a massive success.

Stripe, which was initially built “Only for developers” has now become a financial infrastructure for businesses of all sizes. If you’re a founder or someone who builds stuff on the internet, you probably use Stripe to accept payments, I guessed it right?

The company initially focused on just letting people accept payments, but now it does more than that—From helping people incorporate their business in the US, enabling cross-border payment, funding startups, issuing corporate cards, managing billing and invoices, and much more.

Stripe has truly become the financial infrastructure for businesses online. And this is also why Stripe’s mission is audacious: “To grow the GDP of the internet.” Well, they’re on it: last year in 2024, Stripe did a total of $1.4 trillion in total payment volume, valuing the company at $91.5 billion.

Want to know more about Stripe? Head over to their website.

Ramp

What if you, as a company, want to track and manage all your corporate expenses in one place, and save time and money? This is what Ramp helps you with. It’s a platform that helps you to track and manage your employees' travel expenses, marketing expenses, vendor expenses, bill and invoice payments, and much more, all in one platform.

Ramp, a corporate expense management platform, was founded by Eric Glyman, Karim Atiyeh, and Gene Lee in 2019, aiming to simplify expense management for businesses of all sizes.

The traditional system to manage corporate expenses was broken and inefficient, companies often duck-taping together multiple tools to track all of their corporate expenses and manage them at the same time, which was a disaster, realized by Ramp’s co-founders.

The solution? Building a platform that allows businesses to issue corporate cards and manage their expenses in real time, all in one place, Ramp. But then this begs the question: What makes it unique? First and foremost, the best thing about Ramp is that you can track the expenses in real time. Second, you can set spending limits per person, team, and vendor.

What’s more, you don’t need to ask your employees or team to send you a receipt to keep track of data and the money they spend, so long as they use Ramp Corporate Cards, the process is automated, where every single expense is tracked and completed without you doing anything manually. Here’s how:

Ramp is a powerful, modern expense management platform that every business would love to have in their tech stack. And this is the reason, so far, Ramp is used by 30,000+ customers, including Stripe, Discord, Notion, Webflow, Quora, and more. The company claims that they have saved $2 billion and 20M+ hours over half in the past year, valuing the company at $13 billion.

Ramp says, “Time is money. Save both.” So good.

Chime

One of the biggest problems of relying on traditional banks is their ability to charge you “Makes no sense” money through random, unwanted fees. Traditional banks make fortunes charging their customers monthly fees, overdraft fees, service fees, and many more.

This had to be changed, right? So Chime came along. The company was founded by Chris Britt and Ryan King in 2013, aiming to provide a better banking service to everyday people who live paycheck to paycheck and can’t afford a bank charging them monthly or hidden fees.

Although technically, Chime is not a bank, but it has partnered with some of the trustworthy banks like The Bancorp Bank, N.A., and Stride Bank to work as a neobank. Chime customers aren't big institutions or businesses, but Americans who live paycheck to paycheck and couldn’t bear unwanted fees since it’s their hard-earned money.

Now this begs the question: How does Chime make money? Chime generates its revenue primarily through interchange fees, the fees merchants pay to accept Chime’s card payment. Here, the customer has to lose nothing, the charge is bear by merchants who accept the payments.

Is this working well? Yeah, Chime has a total of ~22 million users, of which 8.6 million are active customers, using Chime as their primary banking platform. The company went public this month on June 12, 2025, with its initial share price at $27, trading at a $16 billion market cap.

Brex

Pretty similar to Ramp but works slightly different. Brex, similar to Ramp, offers corporate cards, expense management, spend control, a travel in-built tool, and business accounts.

While Ramp focuses on helping businesses save money and time, Brex focuses on scalability and flexibility by offering multiple currency support, multiple entities, and localization around the world.

The company was founded by two Brazilian entrepreneurs, Hendrique Dubugras and Pedro Francesch, in 2017, to help small startups, mid-size companies, and enterprises get corporate cards, manage and track their expenses, business accounts, and more.

Brex’s mission:

We're here to empower employees anywhere to make better financial decisions.

Innovative companies today are at the cutting edge of how business gets done. Modern businesses are empowering their teams, automating workflows, digitizing information, and operating globally. They’re doing things differently, inventing new paths, breaking the old way.

Everything about companies has changed, but most financial providers have not. The big businesses of the future are acting more like startups, and traditional banks can't build what they need.

To empower their employees to make better financial decisions that drive the business forward, these companies need financial products that enable their new ways of thinking and keep them growing for the long haul.

So we’re building a first-of-its-kind solution to integrate the financial services and software they’ll need along their way. While they build the future, we’ll be building everything they need to launch confidently, scale smarter, and reach their full potential.

Brex is a successful company with over 30,000+ businesses using the platform, this includes YCombinator, Robinhood, Classpass and more, valuing the company at around $12.3 billion.

Revolut

Revolut's homepage says, “Change the way you money.” That’s powerful, and they mean it. We all know how hard and painful it is (or was) to send or receive money internationally, especially when you travel to different countries.

Traditional banking isn't designed for smooth, fast cross-border payments. They lack innovation, come with high commission and service fees. Co-founders of Revolut realized this and decided to change it.

Revolut was launched by Nikolay Storonsky and Vlad Yatsenko in 2015, aiming to provide a platform to send and receive money abroad effortlessly. They aimed to offer multi-currency accounts, debit cards, commission-free stock trading, business banking, and more, all in one platform.

Initially, the company offered limited products and services, but now? With the help of Revolut, you can send and receive money anywhere in the world, manage your money, get debit cards, invest in crypto, stocks, and commodities, get an eSIM, and much more.

It’s not an American, but a British company that has over 55 million customers worldwide, with more than 11 million from the UK alone. The product is supported in more than 160+ countries and regions. And with that, Revolut is valued at $45 billion, generated over $4 billion in total revenue last year, 2024.

Plaid

Regardless of all these disruptive fintech companies, we haven’t yet fully gotten rid of traditional banking. All the money we send, receive, and transfer, at the end of the day, lands and stores in our traditional bank accounts, right?

But Plaid makes it easier for us, here’s how:

Plaid is a platform for fintech platforms. The company was founded by Zachary Perret and William Hockey in 2012, allowing fintech companies to access customer bank data with ease and effortless. Plaid founders realized that it was so hard to get access to customer bank data and verify them on different fintech platforms.

For example, Robinhood uses Plaid to verify users' bank details and let them deposit or withdraw money on the platform. But if Robinhood didn’t partner with Plaid, it would’ve been hard for them to verify the customer bank details. Robinhood had to partner with each individual bank to do the same thing that Plaid helps them do.

If you’ve ever noticed, when you use platforms like Revolut, Chime, Robinhood, and Venmo to add your bank accounts on the platform, you get to do that easily because those platforms have already partnered with Plaid. That “Fetching” the bank account was impossible without them using Plaid.

So what is Plaid? It’s Zapier but for fintech companies that helps these companies access and track banking details of customers. Plaid has over 100M+ global users’ data, partnered with 12,000+ financial institutions in 17 countries, and more than 8,000 digital finance apps and services use Plaid.

The company is valued at $6.1 billion and generated around $300 million last year.

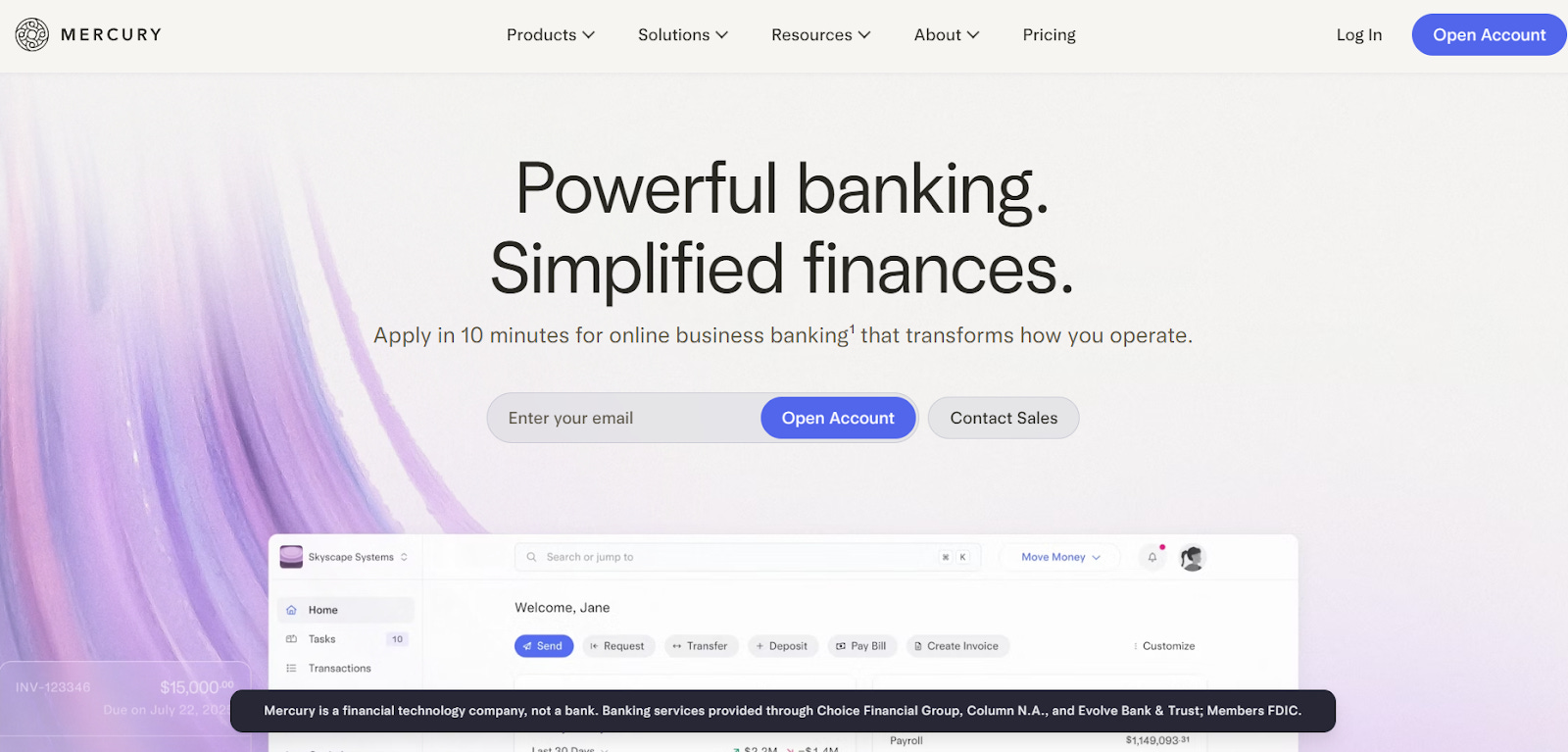

Mercury

Remember, earlier we talked about Chime, which targets everyday people who mostly live paycheck to paycheck? Mercury does the same thing, but targets a different group of people.

Mercury is a platform designed to enable banking services for startups and small companies, helping them open business bank accounts effortlessly and seamlessly online. Mercury, though, is not a bank in itself, but to work as a bank, it has partnered with modern banks.

The company was founded by Immad Akhund, Max Tagher, and Jason Zhang in 2017, aiming to simplify banking services primarily for startups. Founders realized that traditional banks are not designed to help new and mid-tier startups. So when founders started Mercury, they didn’t just focus on its UI and tech, they enabled startups to get access to API, virtual cards, automated cash management, user permissions, seamless integration, and fast customer support.

So far, over 200,000 startups have opened business bank accounts using Mercury, valuing the company at $3.5 billion as of 2025. Well, who needs a Mercury account? If you are a founder who doesn’t want to hassle with traditional banks to open a business account, Mercury is the platform you want to check out.

Mercury helps you open savings and checking accounts, offers credit cards, working capital, provides expense management, invoicing, accounting automation, and more, all in one place.

Thanks for reading, catch you on the next one.

So interesting to see more companies in the space choosing the long game rather than the acquisition game.

Or maybe better put, seeing companies who are strategically determining how to avoid being acquired.

Especially cool what we’re seeing in Latin America.

A very interesting read! They are changing the face of finance as we know it :)

Recently I came across a startup called Thndr, Egypt based fintech democratizing access to investing and advisory. It received funding in May 2025 to further expand.